Buying high and selling low: what aggregate bank flows taught me about investor psychology.

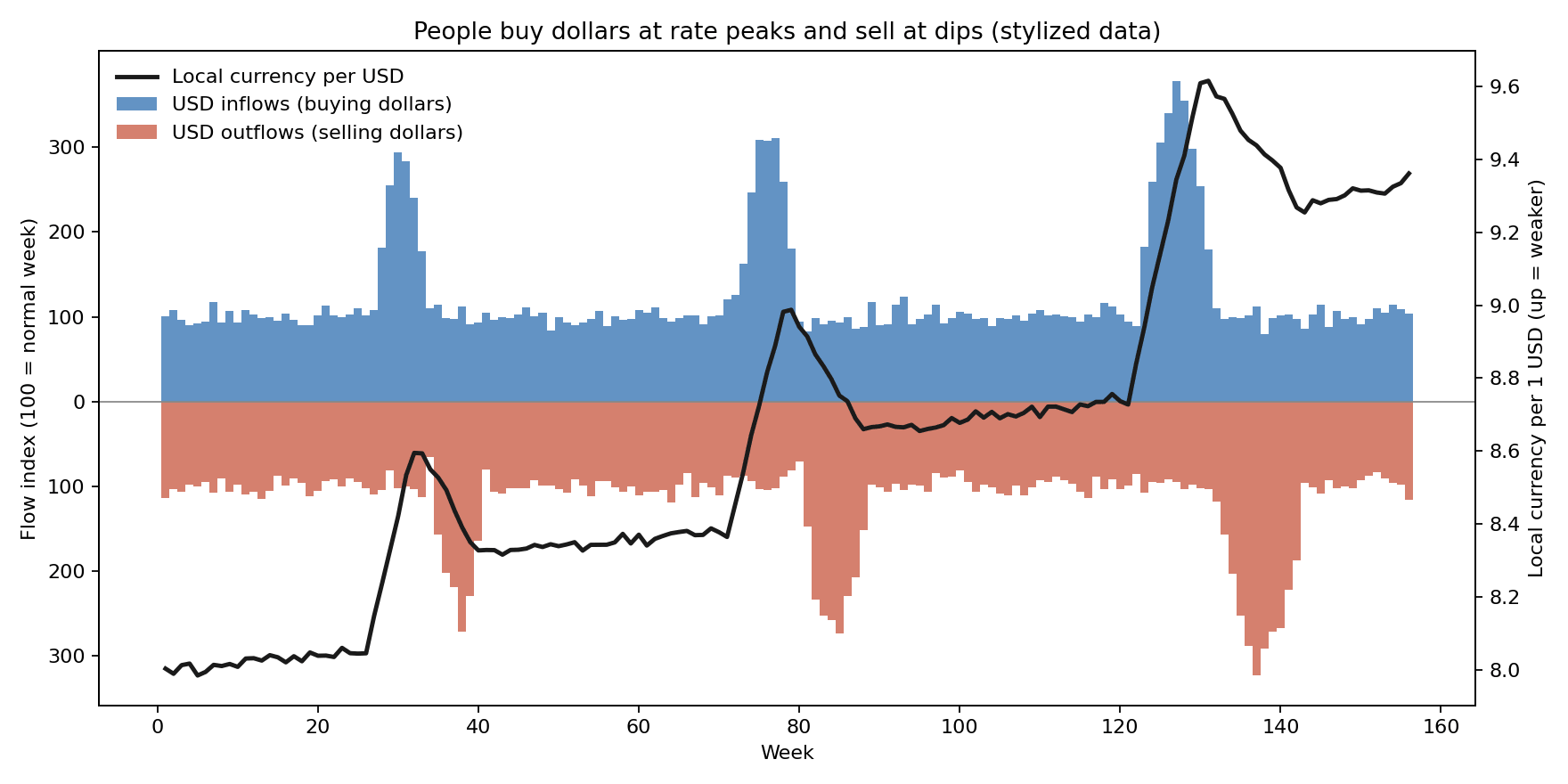

I work in fintech, in the savings domain. I'm also an active stock market investor since 2020, small scale and strictly personal, but enough years to have watched a few cycles and to have caught myself doing some of the things described below. At some point at work I was checking the correlation between dollar balance inflows and outflows against the local currency exchange rate. Nothing fancy, just two time series next to each other. What I found was a pattern so consistent it looked scripted.

Every time the local currency weakened against the dollar, inflows into dollar balances spiked. Every time it strengthened back, outflows spiked. People were buying dollars when they were expensive and selling them when they were cheap. On repeat.

Before you picture a currency crisis: there wasn't one. I observed this over ordinary moves, around 5% down, 5% up. There was no crash or hyperinflation panic, just regular fluctuations that happen a few times a year. And here is the part that makes it worse. The local currency chart against the dollar looks like a mountain ridge that only climbs. It has stable plateaus, sometimes for long stretches, but over any multi-year window it devalues. There has never been a sustained recovery. Selling dollars on a 5% bounce means trading against the entire history of the chart.

A disclaimer before we go further. Everything here is based on aggregate, anonymized flow data, and there are no internal numbers or names in this post. And as you will see below, this pattern is documented across markets and asset classes, so nothing here is unique to any one bank or country. This is also not financial advice; it's a post about psychology.

This is not a local anomaly.

My first thought was that I found something specific to my market. I didn't. Retail investors do this everywhere, with everything.

DALBAR has been comparing market returns with what investors in those markets actually earn since 1985. Their 2024 report: the average equity fund investor made 16.54%, the S&P 500 did 25.02%. That's an 848 basis point gap, or about $850 lost on every $10,000 in a single year. And 2024 wasn't an outlier, it was the fifteenth year in a row that the average investor lost to the index they were holding. The funds weren't the problem. The timing of money moving in and out of them was.

To be fair, DALBAR's math has its critics, and part of that gap comes from how they measure it, not from bad timing alone. Fine. So here's the version with harder math behind it. In 2007, a finance professor named Ilia Dichev asked a simple question: what did investors actually earn, given when they moved their money in and out? He crunched the numbers for nearly every major stock market on the planet and got the same answer everywhere: less than the market itself. Not because they picked bad assets. Because of when they bought and sold them. Stocks, funds, dollars in a savings account, it doesn't matter. Wherever people move money based on recent price moves, they lose to the thing they are holding.

So the question isn't whether people buy high and sell low. They measurably do. The question is why.

The same choice, two different answers.

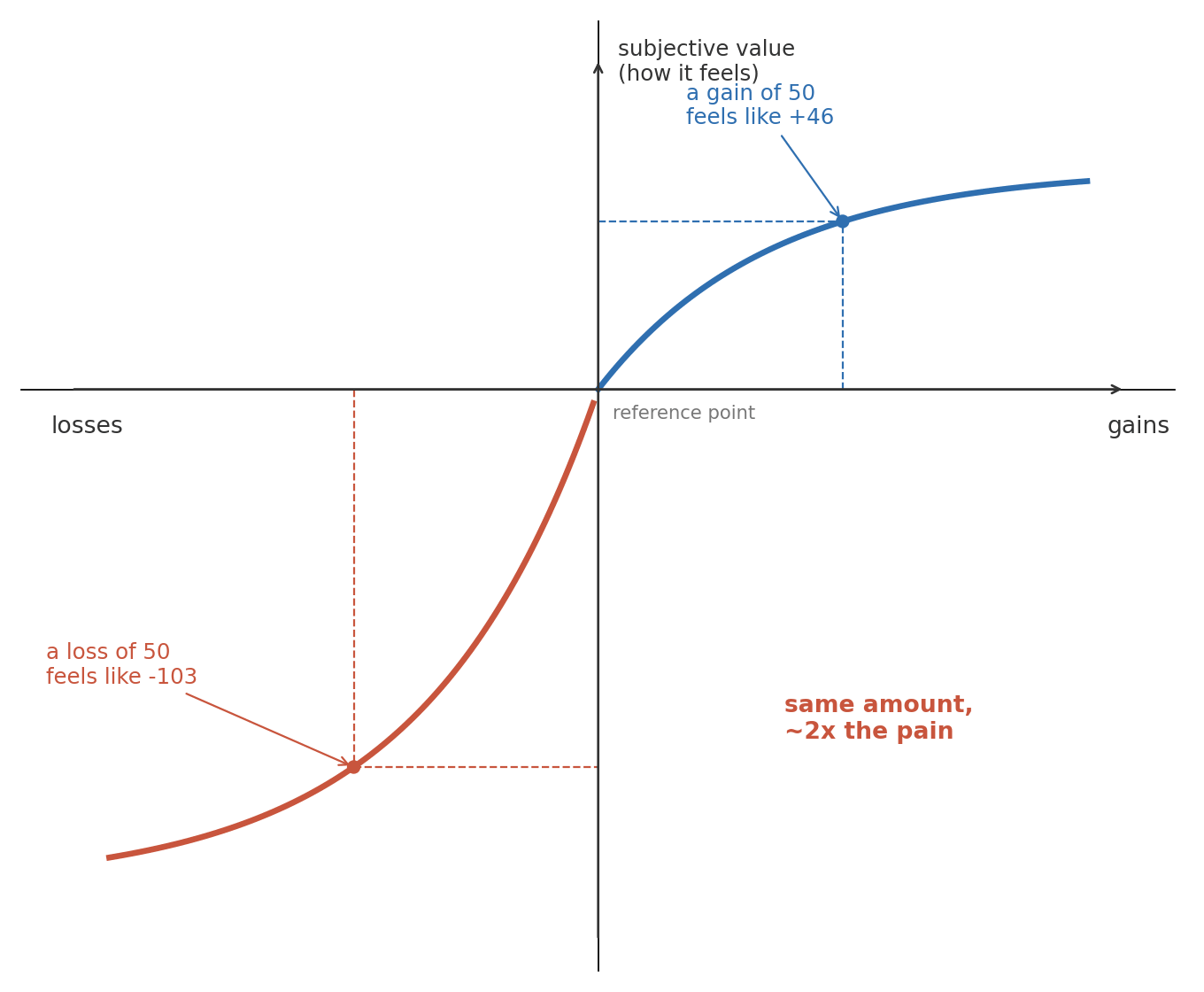

In 1979, Daniel Kahneman and Amos Tversky published prospect theory, and it explains most of what I saw in that flow data. Their core finding: your brain doesn't ask "how much money do I have". It asks "am I winning or losing compared to yesterday", and it treats those two situations completely differently. When a choice feels like a gain, we play it safe and grab the sure thing. When the same choice feels like a loss, we suddenly become gamblers, taking risks just to avoid it.

Their famous demonstration from the 1981 follow-up is the "Asian disease problem." Participants chose between two programs to fight an outbreak threatening 600 people. When options were framed as lives saved, most people picked the certain option: save 200 for sure. When the mathematically identical options were framed as lives lost, most people picked the gamble. Same numbers, opposite preferences. The frame did all the work.

The second finding from prospect theory matters even more here: losses hurt roughly twice as much as equivalent gains feel good. Losing $100 is not the emotional mirror of winning $100. It's about double.

Keep both of those in your head. Loss framing makes us gamble, and losses weigh double. Now back to the flow data.

Why a weakening currency triggers buying.

When the local currency slides 5%, nothing about your salary or your bank balance changed. But the frame changed. Your savings are now "losing" purchasing power against the dollar, and that reads as an active, ongoing loss. Prospect theory predicts exactly what happens next: people staring at a loss start gambling. Converting your savings at the worst rate in months doesn't feel risky in that moment. It feels like stopping the bleeding.

If you have lived through one of those weeks, you know how it goes. Someone at lunch asks if you've converted yet. Your phone shows the rate another percent higher than yesterday. Doing nothing starts to feel like the reckless option.

Attention pours fuel on this. Brad Barber and Terrance Odean showed back in 2008 that regular investors mostly buy whatever is making noise: things in the news, things that just moved sharply. The reason is almost boring. Nobody has time to research every asset in the world, so whatever grabs your attention becomes the menu, and you pick from that menu. An exchange rate is uniquely built for grabbing attention. It's posted on every exchange booth and it enters every office conversation the moment it moves. A 5% slide doesn't need to be a crisis to dominate a week of small talk. And once everyone around you is buying dollars, the cascade feeds itself. The urge to act peaks exactly when the price is worst.

There's also simple extrapolation. A falling rate feels like a trend that will continue, so buying now feels like buying before it gets even more expensive. Sometimes that's even true! But if extrapolation were the real driver, the same people would hold through the recovery, and they don't.

Why they sell when it recovers.

The selling side has its own name: the disposition effect. Terrance Odean tested it in 1998 on trading records from 10,000 brokerage accounts. Investors sold their winners about 1.5 to 2 times more often than their losers. He checked the boring explanations first, taxes and rebalancing and trading costs, and none of them covered it. And it made their returns worse.

Here's how it maps to the dollar savings account. Remember the shape of the chart: the local currency stair-steps down over the years. That means almost anyone who has held dollars for a while is sitting on a gain in local currency terms, and local currency is the unit people think in, because that's what rent and groceries are priced in. Now the local currency strengthens 5%. The gain in that mental account starts shrinking, day by day, with the recent peak as the reference point. The disposition effect predicts what happens next: people rush to realize the gain before more of it evaporates. They convert back and lock it in. In dollar terms, they just sold at a local low.

Against a currency that has only ever stair-stepped downward over the long term, this is remarkable. Every plateau has eventually resolved into another leg down. Selling dollars on the bounce means betting on the one thing the chart has never shown. But the disposition effect doesn't consult charts. It consults the itch to realize a gain while it's still there. Buy in the fear, sell in the relief, lose on both legs of the trip.

The counterargument I have to make.

I can't write this post honestly without the other side. Some dollar buying in weak-currency economies is not a bias at all, it's insurance.

There's a 2024 study by Husnu Dalgic that makes this case well. Currencies like the one I described tend to fall exactly when the local economy is in trouble, which means dollar savings pay out right when your paycheck is at risk. People even accept miserable interest rates on dollar deposits for that safety, basically paying for an insurance policy. Looked at this way, keeping dollars is one of the smartest things a household in a shaky-currency country can do.

But the timing signature separates the hedger from the herd. A rational hedger accumulates dollars steadily, or opportunistically on strength, and holds through fluctuations because the hedge is the point. What I saw in the flow data is the opposite: reactive bursts of buying at local peaks and selling at local dips. That's insurance bought after the flood and cancelled the first sunny week. The asset choice is rational. The timing I saw in the data is not.

What to do about it.

I'm an engineer, so my answer will not surprise anyone who read my other posts: replace in-the-moment judgment with a deterministic rule, decided in advance, when you are calm.

If you want dollar savings as a hedge, pick a fixed amount and convert it on a fixed schedule, regardless of the rate. Dollar-cost averaging is boring and that's the feature. It buys fewer dollars when they're expensive and more when they're cheap, which is the exact inverse of what the flow data shows people doing. Automate it if your bank allows scheduled conversions, because the whole point is to remove the decision from the moment when the loss frame owns your brain.

And if you catch yourself refreshing the exchange rate during a 5% move, feeling that itch to act right now: that itch is the loss frame talking. Kahneman measured it at 2x. It will always feel twice as loud as it deserves to be.

The people in my flow data weren't stupid. They were running default human firmware in an environment built to exploit it. You will not out-think that firmware while the rate is moving. Decide the rules earlier, so the moment has nothing left to decide.

Sources:

- Kahneman and Tversky, Prospect Theory (1979): https://courses.washington.edu/pbafhall/514/514%20Readings/ProspectTheory.pdf

- Odean, Are Investors Reluctant to Realize Their Losses? (1998): https://faculty.haas.berkeley.edu/odean/papers%20current%20versions/areinvestorsreluctant.pdf

- Dichev, Evidence from Dollar-Weighted Returns (2007): https://papers.ssrn.com/sol3/papers.cfm?abstract_id=544142

- Dalgic, Financial Dollarization in Emerging Markets (2024): https://madoc.bib.uni-mannheim.de/66743/1/...ARRANGEMENT-1.pdf

- DALBAR QAIB 2024 numbers: https://www.dalbar.com/press-release/investors-missed-the-best-of-2024s-market-gains-latest-dalbar-investor-behavior-report-finds/

9 Jul

2026